Consider this: Google has invested in flight information provider ITA Software and hotel metasearch engine Room77.

NB: This is an opinion by Richard Vaughton, director at DiscoveryHolidayHomes. It is the second of a two-part series (first article here) looking at the future of hospitality and technology through prism of search and Google.

Hotel chains have also agreed to pilot new schemes with Google to deliver customers directly. These hotels use Google Hotel Finder, Google Business Photos and the Google Wallet payment applications.

Hotel chains are not fond of the aggregators of course and will be watching carefully.

Hotel finder, although quite basic, plays to Booking.com‘s world for book now, but also gives the hotels direct booking details in the same listing, the guest doesn’t have to use any clever search techniques to find it.

A step in the right direction for the inventory managers and only a short hop to book direct online.

However, there is a much more streamlined opportunity for Google and its users, theorised below. Would Google lose its ad client base? Of course not, where else could they go?

Google itself in 2014 has had two great quarters and closed over $30 billion and may be heading to close to $55billion+ for the year.

So the two behemoths of Priceline and Expedia represent 5% of income, not insubstantial, but not life threatening and let’s not forget the Google’s promise:

“Ultimately serve you, rather than our own internal goal or bottom line.”

This is the same situation we find ourselves in. Costs may go up for listings, but pressure from the new potential alternative can alleviate this and allow more “eggs in more baskets” or a wider marketing mix, reducing the hazardous small business risks!

Google already appears to be competing with its own advertisers. This comes full circle to my original problem, just on a much larger scale and with the “ultimate controller” in the driving seat.

We may not have the power to force these changes individually or even as an industry, but Google is at the top of the re-organisation pyramid and has power over all it sees!

The US spends over $4.5 billion on travel advertising last year, over 50% percent was spent on websites and other digital channels, which is substantial.

Of that, hotels spent the most, followed by airlines and online travel agencies.

Analysts suggest that the ad revenue model is less complex for Google and the travel model may require excess resources and dilute Google’s direction.

So they suggest it may be best involved but not at the sharp end.

Senior executives at Expedia and Priceline do not appear concerned; they believe Google may assist their cause via meta-search as they are industry dominant and push hard against the inventory holders!

Metasearch is a wasp’s nest and in itself is not intelligent or experiential, relying on aggregated inventory themselves!

To give a flavour of how much is spent with Google and the income from some of these travel brands, various reports show Priceline and Expedia spent close to $2 billion with Google and income is circa $150 billion from travel bookings.

Customer acquisition costs are high initially but drop with time but search is an ever present opportunity tool for the fickle public.

Bloomberg in 2013 published an article on the “Google Threat” topic.

“From an ad perspective in the travel space, there’s no place to get closer to the transaction than Google,” David Steinberg of XM Marketing Group was quoted as saying. “You’re literally at the transaction.”

Google told Bloomberg:

“We see opportunities to improve the search experience for users searching for travel information on Google.

“We work to continue having productive partnerships with as many online travel companies and industry players as possible.”

Others ponder if Google wants to rely on its big ad spenders forever or if over time it wants to replace them.

When or if?

Admittedly Google is a low key player to date but with their revisions of Google maps and its geo dominance and the growing importance with G+ the writing may be on the wall.

It is the bottom and top of the food chain that is rebelling, so any new opportunity would be well received at polar ends of the rental or full hospitality spectrum.

The perception that Google is huddling up to its big advertisers alienates the Google brand at grass roots level where it wants real traction on social and of course use of its premium tools.

It will see more appreciation and re-kindled “love” and move back to its core values by developing travel technology tools for the individual or small businesses.

This will see more guest interaction within Google’s growing spectrum of products and industries and greater travel satisfaction.

The rental business is much more complex than hotels and because of this the desire to trade directly with its guests is of paramount concern to provide the best experience.

Margins and data complexities do not easily lend themselves to distributed Priceline, Expedia or HomeAway/TripAdvisor-style booking models, despite the pressure to adapt.

TripAdvisor will now take online bookings on its main site for rentals from Holiday Lettings, for example.

Google however is in a perfect situation to be able to develop its travel ambitions within a vast swathe of the rental market and also work with the hotel chains that are determined to be standalone brands.

Google has the opportunity and the ability to create a much richer guest experience by using its data resources to push qualified rental products to potential rental travellers. It is this ability to match guest experience to qualified inventory that makes it so powerful.

Rather than push guest to best margin product without deep data knowledge, push guests to what they really want and with clear selection messages.

For example, 22% of our mailing list are Gmail users and growing rapidly, scale those numbers up and the direct marketing “in-site” and ad opportunities are vast and even greater when combined with intelligent search results.

At the beginning of 2014 Google had over 120 million Drive users with untold amounts of data; it also has over 500 million Gmail users – that’s over 12% of the global population who actually have internet access.

Within key western territories this rises to over 15%.

Where would Google position themselves in the travel industry is the question? They can target exceptionally well. Booking.com simply sends me places I have been to or really bad guesses on where I may want to go! Google probably knows what I had for breakfast and what time my dental appointment is!

Then there are payments, inventory control, data management, feeds and all the headaches in this industry.

However, I use, just an example:

Google Gmail Google calendars Google Street Views Google Earth Google Maps Google Search Webmaster Tools Google Drive And various Google Labs tools YouTube And also commercial apps

If I could add my inventory to a Google Hospitality Engine and use a Google merchant facility, then all my systems can synchronise and are backed up, web based and secure.

We could harmonise booking management or property inventory via an API and Google would make both service subscription income and potential trading commissions or fees from bookings.

This is as close to “direct” as we can get with an intermediary or search engine as everybody’s home page. Google, for all its recent bad press, is still trusted and pan-global, so guests would be happy with a Google brand and transaction or transaction approved trading platform.

Third parties also create some great apps for Google, which means more opportunity for marketing and no walled garden approach as Google owns the entire estate and lets us roam at will.

Apps take it all mobile, so yet another bonus in this fast moving world, but one where Google is no doubt focussed and has concerns. Mobile can sidestep search, so expect mobile acquisitions in travel and Google involvement.

They are already at the technical end with the acquisition of Appurify recently.

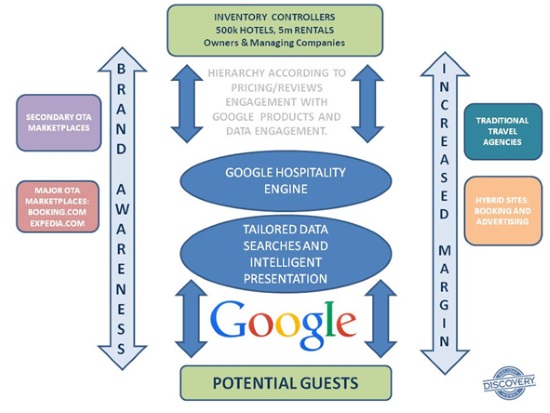

Some of the Google functionality that could be used to enrich a guest’s search experience is shown below; this compliments Google’s vast data knowledge and delivery capacity, matching it to the guest opportunity.

This is our visualisation of a small business relationship with a Google Hospitality model.

The opportunity for Google in travel is immense. Travel involves a great deal of data movement, from flights, to cancelling the daily newspaper. It is also an opportunity for receiving up to date information continually fed into the Google machine by millions of small businesses working at their individual locations.

It will also allow travellers to engage on the move and provide even more real time data. This adds to the global wealth of knowledge, feeding down to a local mobile opportunity for all.

The big aggregation sites are simply catalogues without knowledge and are relatively dormant. Calendars may change but little else, perhaps why Flipkey is looking for expert content contributors.

Google loves engagement and new information, the fresher and varied the better. Owners and managers using a “Google Hospitality Engine” could make full use of its social engagement opportunities and be rated according to this engagement.

The system can drive the reviews process and brings hundreds of thousands of newly engaged Google users. The mere fact that Google manages such a vast network of email users would certainly improve fraudulent review posting!

Perhaps it is my imagination, but the signs may already be there and we can see a move toward intelligent use of data in accommodation provision via Google travel interests or a “Google Hospitality Engine”.

So this time, instead of a A cry from the search wilderness how about “Putting the Good back in Google Travel“.

Come on chaps, help us all out!

NB: The first part of this article is available here.

NB2: This is an opinion by Richard Vaughton, director at DiscoveryHolidayHomes.

NB3: Magnifying glass Google image via Shutterstock.

{kind=link}