While online travel retail sales are continuing their steady growth globally, consolidation is increasing among online travel agencies.

Both Expedia and Priceline are strengthening their positions as the most successful and, some argue, innovative companies, constantly gaining share in the category in the process.

NB: This is a report by Angelo Rossini, online travel analyst at Euromonitor International.

Priceline managed to record the sharpest growth over the 2004-2013 period, which allowed the company to stand beside Expedia at the top of the global online travel agency and travel intermediary ranking in 2013.

Competition between the two OTA giants is getting tougher in 2014, with Priceline continuing its sharp rise and Expedia also achieving a remarkable performance.

The competition between these two companies is expected to remain one of the main themes in the coming years in the online travel sector as it evolves, moving from desktop PCs to mobile devices, from standardised to personalised online marketing, from hotel bookings to include more travel services, and sees the fast rise of Asian customers.

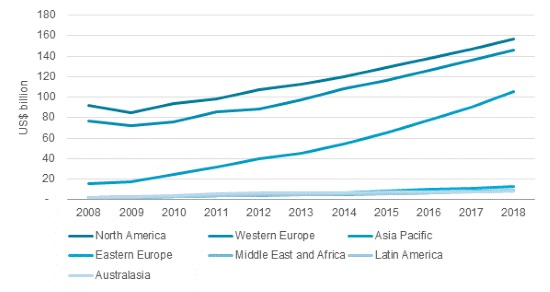

Healthy growth for online travel retail sales driven by Asia-Pacific

Global online travel sales through intermediaries recorded another strong performance in 2013, when they grew by 9%.

During the 2013-2018 period, growth is expected to stay steady, driven by the Asia Pacific region.

Online travel retail sales are expected to grow at an 18% compound annual growth rate (CAGR) in Asia-Pacific over 2013-2018, thanks to the increasing penetration of ecommerce, and especially mobile commerce, among growing affluent and middle classes in the region.

Online travel retail sales by region: 2008-2018

Expedia and Priceline drive consolidation in the OTA sector

The sharp rise in online travel retail sales in the past 10 years has put Expedia and Priceline at the top of the ranking of travel intermediaries, ahead of traditional players across both leisure and corporate travel such as Carlson Wagonlit Travel, TUI Travel, American Express and Thomas Cook.

The success of Expedia and Priceline is also driving strong consolidation in the online travel agency category, with them well ahead of their competitors in terms of both sales and as engines of innovation.

While both companies saw strong growth in terms of gross bookings in 2013, some of their main competitors suffered poor performances in the same year.

In particular, the other two big US OTAs, Orbitz and Travelocity by Sabre (now essentially an affiliate of Expedia), suffered stagnation and a strong decline in sales respectively.

Top global online travel agencies by value sales: 2012-2013

Priceline reaches the top of the rankings in 2013

Over the course of 2013, Priceline reached Expedia at the top of the OTA and travel intermediaries ranking, generating US$39 billion in terms of gross bookings.

In spite of Expedia’s good performance during the year (+16%), the last of a long list of very strong performances by Priceline (+38%) allowed it to reach its rival in terms of gross bookings.

Competition gets tougher in 2014

Competition between the two OTA giants is getting tougher in 2014. Results for H1 2014 saw the two companies very close in terms of gross bookings, with Priceline generating $25.8 billion (+34%) and Expedia standing at $25.7 billion (+29%).

Priceline recovered much ground from Expedia over 2004-2013 thanks to its more flexible agency model, larger online advertising investments (mainly on Google paid search results) and stronger expansion in international markets, first with Booking.com in Europe and then with Agoda in Asia Pacific.

The agency model allows customers to pay directly in hotels and to, generally, easily cancel their reservation, while the merchant model offers consumers less flexibility and requires prepayment to the OTA.

However, the pattern of the first six months of 2014 seems a bit different, with robust growth in Expedia’s sales. A strong domestic performance has been driven by the migration of the US and Canadian Travelocity brand’s sales to the Expedia platform.

Moreover, the launch of the Expedia Traveler Preference Program, allowing consumers to choose between prepayment and payment at the hotel, has made Expedia’s offer more flexible and better positioned to compete with Priceline’s agency model.

The agency model accounted for 83% of Priceline’s sales in 2013, largely due to this model being used by its Booking.com subsidiary.

Sales through the agency model drove Expedia’s sales growth in H1 2014, recording a 38% rise, while merchant model sales grew by a lower 18%.

Now approved by the Australian Competition and Consumer Commission, the acquisition by Expedia of the leading Australian OTA, Wotif, will be another significant step towards strengthening the global position of the company.

Competition moves East

An important battleground for the global competition between Expedia and Priceline today is China. The online travel market in the country is currently exploding and as Priceline’s President and CEO Darren Huston has stated that in “five or ten years down the road it will be hard to say you are global if you are not big in China”.

Asia Pacific companies such as leading Chinese OTA Ctrip and Indian leader MakeMyTrip appear the only ones among the world’s leading OTAs currently able to challenge the pace of growth of Priceline and Expedia.

Ctrip recorded 29% growth in terms of gross bookings in 2013, while MakeMyTrip saw 15% growth.

In August 2014 Priceline expanded its partnership with Ctrip, started in 2012, through a US$500 million investment that will eventually give the company ownership of 10% of Ctrip shares.

On the other hand, Expedia has full control of eLong, the number three Chinese OTA, which is its arm for expansion in this booming market.

Focusing on mobile channel and personalised marketing to stay ahead in innovation

The Expedia and Priceline leadership in the OTA sector as well as their strength in dealing with direct suppliers such as hotel chains seems very likely to continue in the coming years thanks to the ability of these two companies to stay well ahead of other travel players in terms of innovation.

Expedia’s strategy is focusing on building a flexible architecture allowing consumers to book and receive assistance on multiple devices, including wearable electronics, and on personalisation powered by big data analytics, in order to offer, in the words of Expedia CEO Dara Khosrowshahi, “the possibility to show very specific deals to small segments of the population”, going beyond rate parity and increasingly partnering with hotel chains to do that.

Priceline’s strategy is equally focused on mobile devices in order to offer its customers the possibility of making their bookings wherever they are through smartphones, tablets, connected cars and in-flight screens, recognising that the mobile channel has deeply changed consumer behaviour in the travel industry.

Personalisation of online marketing is also progressing steadily at the company through e-mail marketing and customised suggestions for customers.

Mobile booking of in-destination services and B2B move in Priceline’s strategy

The focus on the mobile channel is also behind Priceline’s US$2.6 billion acquisition of OpenTable, an online restaurant reservations company.

The gradual evolution of online travel agencies into mobile travel agencies expected in the next few years will mean that they will increasingly become platforms for mobile reservations for travellers on the go, which will go beyond the hotel booking to include other tourist services, such as meals and tourist activities.

Moreover, Priceline is also focusing on its role of online hotel reservations champion to offer B2B online marketing services to hotel chains, taking care of the whole marketing and booking process for them.

This strategy is behind the acquisitions in June 2014 of B2B hotel marketing brands Hotel Ninjas and Buuteeq.

Both Expedia and Priceline are also investing in the promotion of their Trivago and Kayak metasearch engines, with this being a growing sector in the travel industry, which also allows them to rely less on Google advertising investments.

The fast pace of innovation led by the two OTA leaders promises very dynamic years ahead, which will no doubt see significant changes in online travel, meaning that the ability of market players to be swift to adapt to them will be increasingly key.

Stronger cooperation between online travel intermediaries and suppliers as well as with technology companies appears likely in the coming years in order to be competitive in addressing increasingly sophisticated consumer demands.

NB: This is a report by Angelo Rossini, online travel analyst at Euromonitor International.

{kind=link}